The Waldorf Astoria, NYC courtesy of Alan Light, CC BY 2.0.

The real estate conferences for the year have kicked off. I started the year off by attending the Goodwin Proctor Real Estate Capital Markets Conference held at the beautiful Waldorf Astoria Hotel in New York City on January 30.

The first session was on real estate fundamentals and included panelists representing JPMorgan Asset Management, Chandan Economics, and Prudential Annuities, among others. A few of the key takeaways are that Hilary Spann, Executive Director of Northeast Real Estate Acquisitions for JPMorgan Asset Management, said that her firm is forecasting the 10-year Treasury yield to be 4% in their long-run models. The panel also acknowledged that there is a low correlation between movements in the 10-year Treasury yield and movements in other fundamental commercial real estate indicators.

The second panel, entitled “On the Ground: Public and Private Real Estate Capital Markets,” focused on the investment side of real estate. The all-female panel included representatives from Canopy Investment Advisors, Park Madison Partners, and W.P. Carey. In terms of real estate investment advice for 2015, one of the panelists said she was focusing on urban areas with high barriers to entry, housing assets that can be bought at a discount relative to the asset’s reconstruction cost, and particular European markets where office rents are off significantly compared to their peak.

Another panelist focused her discussion on the continuing trend of increases in operational due diligence, which manifests as more site visits prior to the acquisition of an asset and more scrutiny of the numbers behind the deal. Investors want firms that have very good due diligence practices, which are often driven by the folks managing the deals. According to another panelist, investors want the best deal managers in terms of performance, and then they generally worry about fee structures.

At the end of the panel, one of the panelists asked the audience members to raise their hands if they had participated in a crowdfunded real estate deal. Less than 1% of the audience acknowledged having participated in a crowdfunded deal. Given some of our other research on crowdfunding, it will be interesting to see how this changes in the coming years.

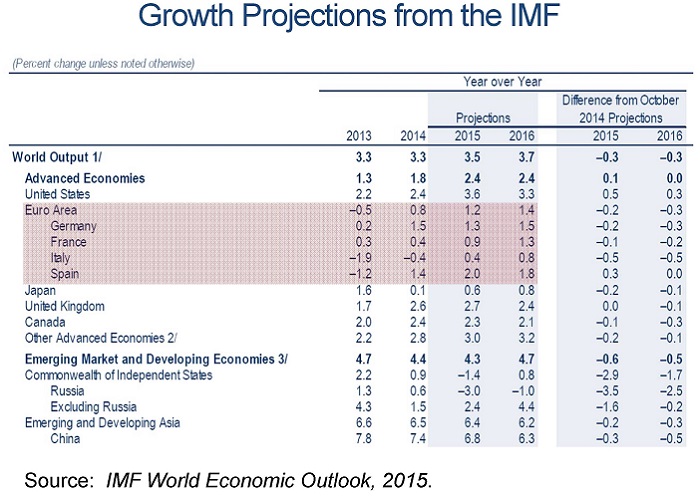

Finally, the keynote address just before lunch was given by Christina Romer, former Chair of the White House Council of Economic Advisers in the Obama Administration and currently the Class of 1957 – Garff B. Wilson Professor of Economics at the University of California, Berkeley. In her 2015 outlook, Dr. Romer noted that there is a mixture of good economic news and bad economic news. The good news includes the increases in non-farm employment, strong GDP growth in 2014 (primarily due to increases in consumer spending), consumer confidence, and lower oil and gas prices. The bad news includes the level of real GDP, the level of employment, GDP growth in Europe, and the downshifting of GDP growth in China (from double-digit yearly growth to 7.4% in 2014).

Growth Projections slide from Dr. Romer’s presentation.

Toward the end, Dr. Romer discussed how the mixture of good and bad news would influence macroeconomic policy. The European Central Bank just started its own quantitative easing (QE) program, which will have global ramifications. China’s investment in high-speed rail and other infrastructure improvements made in the last 5 years seems to be slowing down, which will have additional impacts on its GDP growth rates in the coming years. In terms of U.S. monetary policy, the Federal Reserve has signaled that June 2015 is when it is likely to start increasing interest rates. But the problem with that, according to Romer, is that other indicators (e.g., unemployment) may not support or provide the foundation for increased interest rates. Also, the U.S. dollar has appreciated approximately 15% in the last 6 months, which keeps inflation at bay. Romer also thinks that interest rates will not start to increase in June 2015, but that September 2015 is more likely.

{kind=link}

Recent Comments