Last week I attended the third International Conference on Housing Risk, presented by the American Enterprise Institute (AEI) International Center on Housing Risk in conjunction with the Collateral Risk Network. Day 1 focused on the various metrics used to measure risk objectively. Risk spans the gamut from individual risk to foreclosure risk and everything in between. Risk, then, is affected by different kinds of leverage. [Edward Pinto, AEI, lists nine different kinds of leverage involved in the mortgage origination process.]

What seems to be a paradigm shift of sorts (a la Thomas Kuhn’s 1962 book entitled The Structure of Scientific Revolutions) is a movement from the simple reporting of average risk rates among groups of people or groups of locations (e.g., ZIP codes or metropolitan statistical areas [MSAs]) to individual level measures of risk. This is not unlike the movement of property valuations in the early 1990s from reporting statistics for properties that had transacted in a market to statistics on properties that had not transacted but for which valuations could be estimated (e.g., using automated valuation models or AVMs).

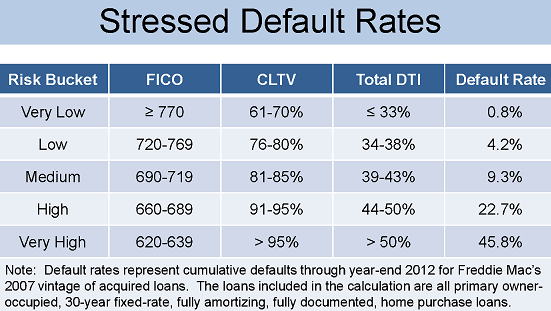

Stressed default rates table courtesy of Edward Pinto.

Several of the metrics used to assess risk include the Housing Cycle Risk Index (John Burns Real Estate Consulting), the National Mortgage Risk Index (AEI), the Housing Credit Index (CoreLogic), and others. Each of these indices measures something different and has its own data requirements.

Folks familiar with finance will recognize the concept of “beta” used to measure the riskiness of an investment or an individual stock. CoreLogic’s Michael Bradley described how his firm uses the concept of “beta” to measure the risk associated with lending on a particular property, given the characteristics of the loan made to purchase the property and the characteristics of the borrower (also known as the mortgagor).

Another interesting discussion from Day 1 was the idea of separating the total value of a property into the value of the land and the value of the improvements. Appraisers have been doing this in the cost approach to value for many years. Specifically, the consensus of the panelists is that the volatility of land values is greater than the volatility of the improvement values. This is important for several reasons.

First, this is important in the formulation of hedonic price indexes, which are used by researchers to measure changes in prices over time and are useful in controlling for individual differences in the dwelling and location characteristics of properties.

Second, this is important because the use of the cost approach in form appraisals seems to have decreased in recent years. Oftentimes appraisers will determine the value of a property, for example using the sales comparison approach, and then “back in” to the land value (often called the site value) after they compute the replacement cost of the improvements on a piece of property. This is not consistent with good appraisal practice.

Stay tuned for more summaries from the International Conference on Housing Risk as well as ABS East.

{kind=link}

Recent Comments